Village Board to discuss 2024 Tax Levy options

HUNTLEY — At the Nov. 7 Village Board meeting, the Village Board must approve the annual property tax levy in sufficient time to file the approved property tax levy ordinance with the County Clerk’s Office by Dec. 31.

According to village staff, the 2024 estimated Rate Setting Equalized Assessed Valuation (EAV) increased by 14.7% from last year. The growth in EAV is attributable to the appreciation of existing properties and new construction. The EAV of new construction totals 2% of the total EAV and could provide $125,300 in additional financial resources using the current tax rate.

In addition, existing property values appreciated 12.3% across all property types and are used to estimate tax bills. A property with a $325,000 market value in 2023 is estimated to appreciate $364,922 in 2024. Properties that appreciated less than 12.3% may see a lower-than-estimated tax bill. Properties that appreciated more than 12.3% may see a higher-than-estimated tax bill.

Three levy options will be presented to the Village Board to choose from. Option One proposes a levy of $5,295,424 and represents a 0% change from 2024. The limited rate would decrease 12.8% from 0.43 to 0.37 per $100 of assessed valuation. No new growth would be captured but would instead contribute to lowering existing tax bills since levying the same dollars across more properties decreases the average tax paid on all properties.

Option One would meet the village’s policy of keeping the tax rate low and funding the village’s Police Pension but would decrease available financial resources for General Fund operations by 6.2%. This option would also direct 32.2% of the levy to the Police Pension compared to 28.6% in 2023.

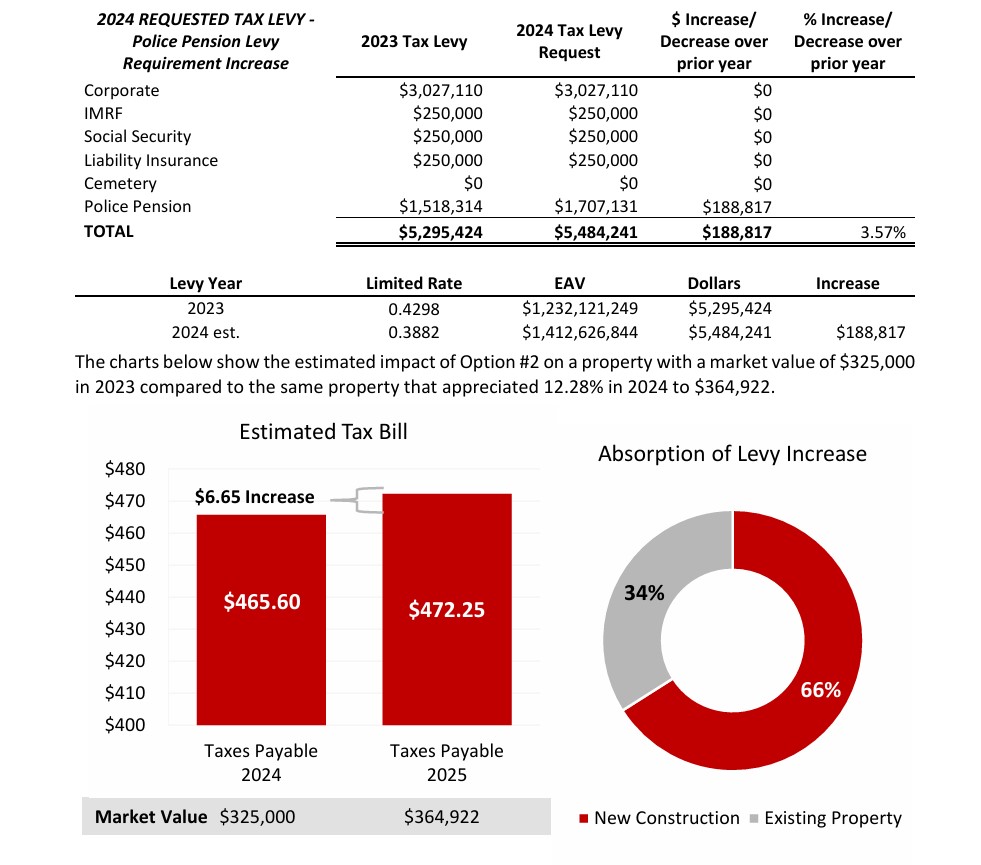

Option Two proposes a levy of $5,484,241 and represents a $188,817 or a 3.6% increase from 2023 which is the increase in the Police Pension. The limited rate will decrease by 9.7% from 0.43 to 0.39 per $100 of assessed valuation. New construction absorbs 66% ($125,300) and existing property absorbs 34% ($63,517) of the levy increase.

Option Two also meets the village’s policy of keeping the tax rate low while meeting the village’s policy of funding the Police Pension; however, it does not increase financial resources for General Fund Operations. This option directs 31.1% of the levy to the Police Pension compared to 28.6% in 2023.

One thing to note about this option is that the Fiscal Year 2025 Draft Budget was formed around Option Two and was the option selected last year.

Option Three proposes a levy of $6,071,203 and represents a $775,779 or 14.65% increase from last year. The limited rate will remain at 0.43 per $100 of assessed valuation. New construction absorbs 16% ($125,300) and existing property absorbs 84% ($650,479) of the levy increase.

Option Three would require the village to post the “Black Box” notification per the Truth in Taxation Guidelines. This essential means that the village must publish a notice in a newspaper and a public hearing must be held if the proposed aggregate tax levy is more than 5% greater than the previous year’s tax extension.

This option meets the village’s policy of keeping the tax rate low by keeping the limited rate the same as last year and covers the village’s Police Pension while adding $586,926 in financial resources for the General Fund. This option directs 28.1% of the levy to the Police Pension compared to 28.6% in 2023.

Staff is requesting that the Village Board choose a policy direction for the 2024 tax levy for taxes payable in 2025 based on the three options that will be presented at the Nov. 7 Village Board meeting.